Briefing

- Asian equity markets traded mixed as investors monitored the Trump-Xi summit in Beijing and ongoing Iran ceasefire uncertainty.

- Wall Street overcame those headwinds to post record highs, with the S&P 500 and Nasdaq closing at new peaks despite accelerating PPI inflation data.

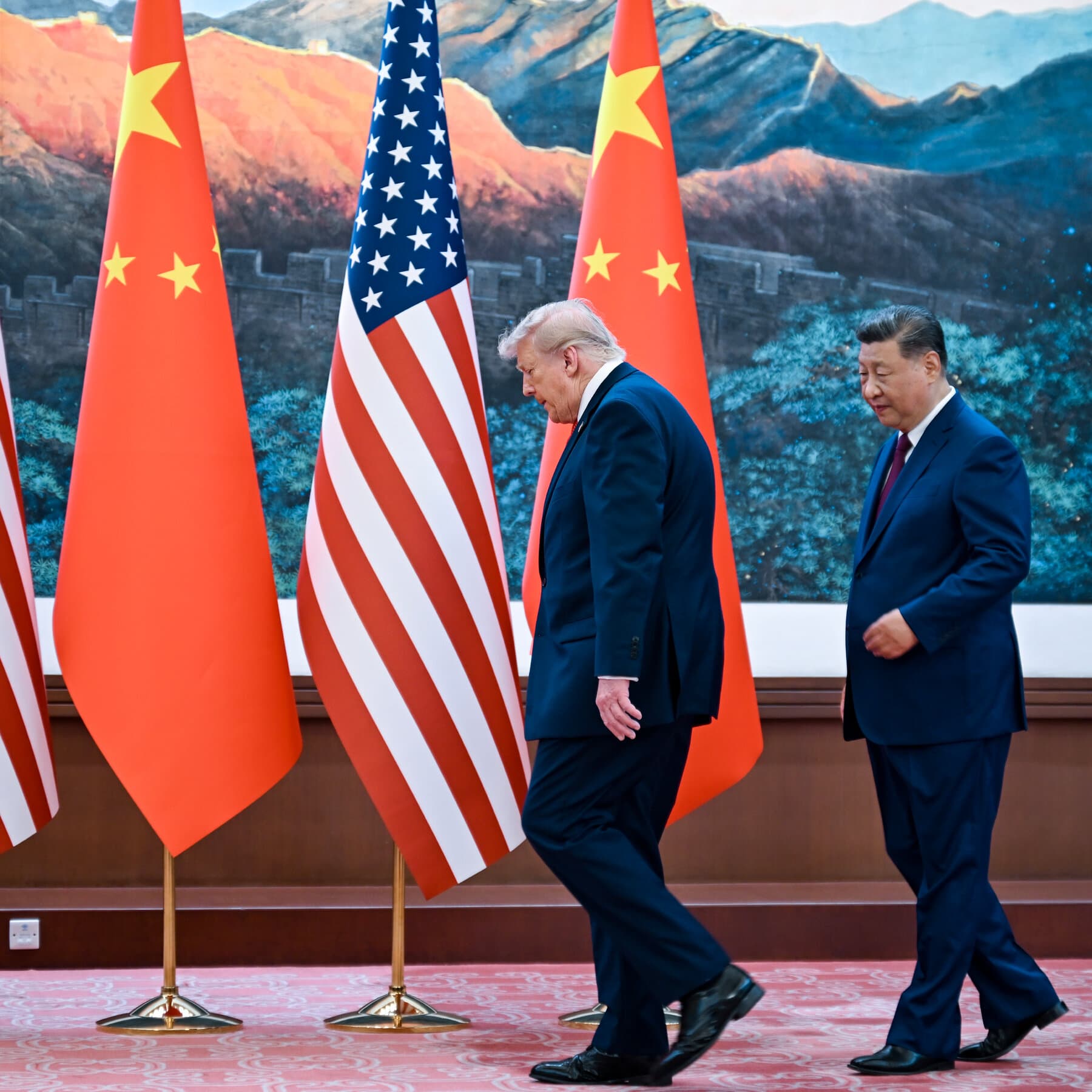

- Trump arrived in Beijing accompanied by major technology executives including Nvidia CEO Jensen Huang, adding a trade and tech dimension to the summit.

- The Iran ceasefire remains fragile, described as being on 'life support', though markets largely looked past the uncertainty in the prior session.

- Stock futures ticked higher with the AI trade back in focus, as investors assessed potential outcomes from the Trump-Xi talks for clues on US-China ties.

- PPI data accelerated, reinforcing concerns about sticky inflation in the US even as equity markets shrugged off the print.

Analysis

- The Iran ceasefire reversal compounds the 3.8% April CPI print into a stagflationary feedback loop: energy prices stay elevated, the Fed under Warsh holds rates, and rate-sensitive Asian equities face a dual headwind of higher-for-longer US rates and regional supply chain disruption. The Calbee naphtha shortage illustrates how Hormuz-linked energy costs are already propagating into manufacturing input costs across Japan and Asia ex-China, pressuring consumer staples margins beyond just energy sector names.

- The pause in the AI chip rally, arriving simultaneously with Burry's parabolic tech warning and a hotter CPI print that removes near-term Fed cut optionality, raises the probability of a broader unwind in high-momentum AI hardware names across Asian markets. TSMC and SK Hynix, which have run on AI demand optimism, face a sentiment reversal catalyst precisely when the macro backdrop tightens: no rate relief, no Iran de-escalation, and Burry flagging crowding risk in the same names.

- The Trump-Xi summit now carries binary risk for Nvidia and the broader semiconductor complex: Jensen Huang's last-minute inclusion creates a direct lobbying channel on AI chip export restrictions, but the record China trade surplus arriving at the summit table gives US negotiators reason to withhold semiconductor concessions as leverage. A failure to secure export relief at the summit would lock in the China revenue gap for Nvidia through the remainder of 2026.

Historical Context

- 2022

The 2022 Hormuz-adjacent Gulf disruption fears and post-Ukraine energy shock produced a similar stagflationary combination of elevated energy-driven CPI and a Fed forced into aggressive tightening, crushing both rate-sensitive equities and Asian technology stocks simultaneously as dollar strength compounded regional selling pressure.

- 2019 Hormuz

Iran's seizure of tankers in the Strait of Hormuz in mid-2019 briefly spiked Brent by 4% in a single session and triggered risk-off moves in Asian equities, demonstrating how ceasefire fragility translates mechanically into energy price volatility and regional equity selling within hours of escalation headlines.

- 1990 Gulf War

Iraq's invasion of Kuwait triggered an oil price spike that pushed US CPI above 6% and contributed to the 1990-91 recession. The mechanical link to this story is direct: a Middle East supply shock feeding into energy-led CPI forces the Fed into a hold or tightening posture regardless of underlying growth, the same transmission channel operating now.

Connected Events

US inflation hits 3.8% in April, highest since 2023

US April CPI hitting 3.8%, its highest since 2023, driven primarily by Iran-war energy costs, directly removes Fed rate cut optionality and reinforces the dual headwind identified in today's Asian equity selloff.

Calbee switches to monochrome packaging as Iran war disrupts ink supply chain

Calbee switching to monochrome packaging due to Iran-war naphtha shortages demonstrates that Hormuz disruption is already propagating through petrochemical supply chains into Asian consumer goods manufacturing, compounding the risk-off pressure visible in regional equities today.

Jensen Huang joins Trump's China delegation as last-minute addition

Jensen Huang's last-minute addition to the Trump China delegation introduces a semiconductor-specific wildcard to the Trump-Xi summit that investors are monitoring for trade policy signals, directly relevant to the positioning uncertainty flagged in today's Asian market selloff.

Further reading

See Indexa more often on Google

Mark Indexa as a preferred source — your Top Stories will surface more Indexa coverage.